The EMR/EHR market in 2026: Who dominates and why

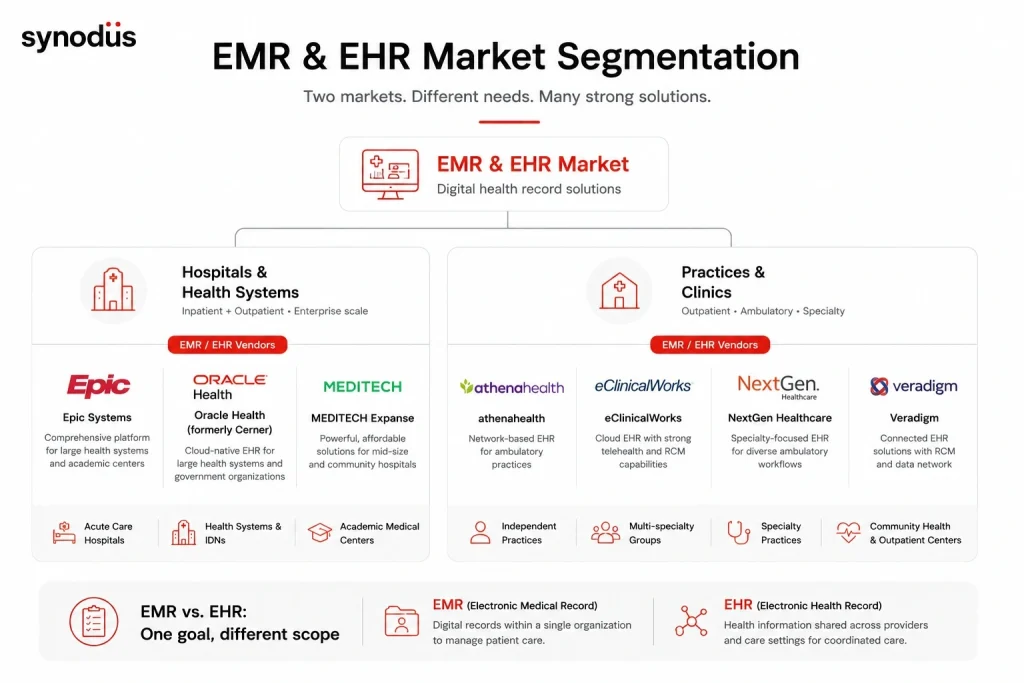

Three companies dominate the US acute care hospital segment:

Epic Systems commands 41.3% market share, Oracle Health (formerly Cerner) holds 21.8%, and MEDITECH holds 11.9%. These three together control roughly 75% of the acute care hospital market.

The ambulatory and physician practice segment is more fragmented, with eClinicalWorks, Athenahealth, NextGen, Veradigm, Greenway Health, and dozens of specialty-specific vendors competing for market share.

Ambulatory and physician clinics are growing at a 6.09% CAGR through 2031 – faster than the hospital segment – driven by digitalization mandates, telehealth integration, and the shift to value-based care arrangements that require quality reporting infrastructure.

Asia-Pacific is on track for a 6.99% CAGR through 2031, the fastest-growing region globally, as government digital health initiatives and hospital digitalization programs drive adoption in Vietnam, the Philippines, Malaysia, Indonesia, and India.

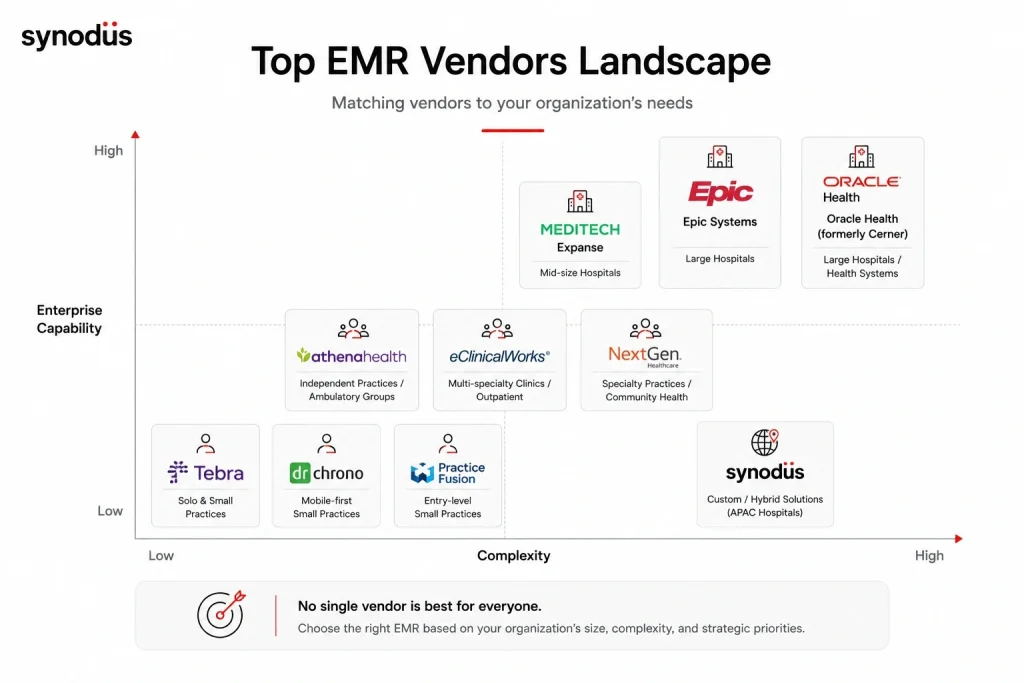

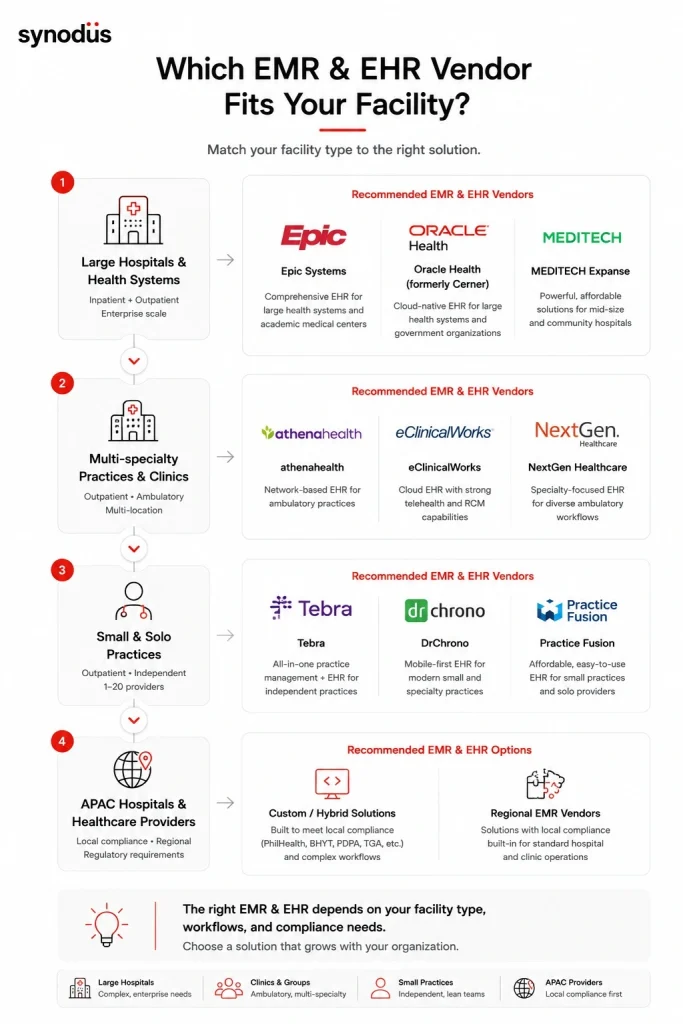

Top EMR and EHR companies for large hospitals and health systems

1. Epic Systems

Epic is the undisputed market leader for large health systems. Known for its comprehensive, deeply integrated platform for large health systems and academic medical centers, Epic consistently gains market share due to its reputation for robust clinical documentation and integration.

Epic’s MyChart patient portal serves hundreds of millions of patients globally. Its app marketplace hosts thousands of third-party integrations. In 2024, Epic adopted USCDI v3 federal data exchange standards ahead of the December 2025 deadline and added a net 176 hospitals – its largest annual gain on record.

Strengths: Unmatched depth and ecosystem, best-in-class interoperability, AI-assisted ambient documentation, largest third-party app marketplace.

Limitations: Implementation cost runs $15 million or more for mid-to-large hospitals with timelines of 12-24 months. Not practical for organizations without substantial IT infrastructure and dedicated implementation resources.

Best for: Large hospital networks, academic medical centers, and integrated delivery networks in North America and select international markets.

2. Oracle Health (formerly Cerner)

Oracle Health holds 21.8% market share. Following a $28.3 billion acquisition by Oracle, the company combines Cerner’s deep healthcare expertise with Oracle’s cloud infrastructure. It has a strong historical foothold in large-scale government contracts, including the Department of Veterans Affairs.

In 2025, Oracle launched a cloud-native EHR with an embedded “Clinical AI Agent” – ambient listening that auto-generates structured clinical notes. Early reports show meaningful documentation time reductions. Oracle lost a net 74 hospitals in 2024 following a difficult post-acquisition transition period, but their cloud-native architecture and AI documentation tools are rebuilding momentum.

Strengths: Cloud-native OCI infrastructure, AI-powered documentation, strong government and VA relationships, lower TCO trajectory than Epic for cloud-first organizations.

Limitations: Post-acquisition transition damaged trust with some clients. Implementation consistency has been uneven. Oracle declined to share new contract lists with KLAS in 2024.

Best for: Large health systems already in the Oracle ecosystem, government-affiliated hospitals, and organizations prioritizing cloud-native infrastructure.

3. MEDITECH Expanse

MEDITECH holds 11.9% market share and is a powerful contender for its target market, combining affordability, comprehensive functionality, and improved user experience.

MEDITECH has ranked in the KLAS top two for mid-size hospitals (151-400 beds) for five consecutive years. Their MaaS (MEDITECH-as-a-Service) cloud model delivers enterprise-grade functionality without requiring large IT teams or capital infrastructure. In 2025 alone, 15 rural hospitals selected MEDITECH Expanse specifically for this reason.

Strengths: Strong KLAS ratings for mid-size segment, cloud-native MaaS reduces infrastructure burden, AI-assisted documentation including ambient listening and auto-generated discharge summaries.

Limitations: Limited customization for complex specialty needs. Analytics tools solid but not best-in-class. No public API.

Best for: Community hospitals, regional health systems, and rural hospitals in the 100-500 bed range.

Top EMR and EHR companies for ambulatory and multi-specialty practices

4. eClinicalWorks

eClinicalWorks serves over 180,000 healthcare professionals across ambulatory and hospital settings. Cloud-based, with strong telehealth integration, population health tools, revenue cycle management, and AI-assisted documentation. Competitively priced for the mid-market.

Its healow patient engagement platform covers appointment scheduling, telehealth, and patient communication across multiple channels. The 2025 release of its AI Scribe – ambient listening for automatic clinical note generation – has been widely adopted among existing clients.

Strengths: Large US user base, competitive pricing, strong telehealth integration, broad ambulatory feature set, active development roadmap.

Limitations: Better suited for outpatient than inpatient care. Has faced regulatory scrutiny in the past over data accuracy issues – worth researching before committing.

Best for: Multi-specialty clinics, outpatient facilities, and telehealth-forward organizations in the US market.

5. Athenahealth

Athenahealth’s “athenaNet” network-based model is its primary differentiator: because all clients share one platform, billing rule improvements, coding accuracy updates, and regulatory compliance changes are applied across the entire client base automatically.

Its 2025 launch of athenaAmbient – AI ambient scribe integration – adds real-time clinical note generation during patient encounters. Strong patient engagement tools and a network of 160,000+ providers support care coordination across practices.

Strengths: Network learning model improves billing and compliance automatically, strong patient engagement, athenaAmbient for documentation, large provider network.

Limitations: Not a full inpatient solution. US-centric – limited localization for international markets. Some users report customer support quality inconsistency.

Best for: Independent practices, multi-specialty ambulatory groups, and outpatient organizations looking to reduce administrative burden without large IT overhead.

6. NextGen Healthcare

NextGen serves ambulatory practices and community health centers, with particular strength in specialty-specific workflows. Their NextGen Office cloud EMR targets small practices; NextGen Enterprise serves mid-to-large ambulatory organizations. Strong in specialties including behavioral health, OB/GYN, and orthopedics.

In 2025, NextGen added AI-powered ambient documentation and enhanced population health analytics, strengthening its position in value-based care programs.

Strengths: Deep specialty workflow support, strong community health center experience, solid revenue cycle management, active FHIR interoperability development.

Limitations: Interface can feel dated in older versions. Implementation complexity varies by product tier.

Best for: Specialty practices, community health centers, and ambulatory organizations in value-based care programs.

7. Veradigm (formerly Allscripts)

Veradigm focuses on ambulatory care and clinical data networks. Their platform covers practice management, EHR for outpatient settings, medication management, and population health analytics. Their differentiated value is network connectivity – real-time data exchange across care settings for multi-site ambulatory groups.

Strengths: Strong ambulatory workflow coverage, network-connected data exchange, solid revenue cycle tools, population health analytics.

Limitations: Not a full inpatient HIS. Following the Allscripts rebrand, some clients have reported service transition issues. Weaker presence in APAC and international markets.

Best for: Multi-site ambulatory networks and outpatient-heavy organizations prioritizing revenue cycle and clinical data exchange.

Top EMR/EHR companies for small and solo practices

8. Tebra (formerly Kareo + PatientPop)

Tebra is built specifically for independent practices – solo physicians, small groups, and specialty practices that need a complete practice management and EMR solution without enterprise complexity. Covers clinical documentation, scheduling, billing, patient engagement, and marketing tools in one platform.

Their 2025 AI Note Assist generates structured SOAP notes from ambient listening, reducing documentation time significantly for small practices where every minute matters.

Strengths: Purpose-built for independent practices, intuitive interface, integrated patient acquisition and marketing tools, competitive pricing, strong customer support reputation.

Limitations: Less suited for practices scaling to 20+ providers. Limited specialty-specific depth compared to dedicated specialty platforms.

Best for: Solo physicians, small independent practices, and specialty practices that want a complete practice management solution without enterprise overhead.

9. DrChrono

DrChrono is a cloud-based EMR designed for modern practices, with native iPad and iPhone integration that allows clinical documentation directly from mobile devices. Strong in ambulatory and specialty settings, with a customizable clinical form builder that lets practices design documentation workflows without developer involvement.

Strengths: Mobile-first design, customizable forms, competitive pricing, strong telehealth integration, open API for third-party integrations.

Limitations: Fewer advanced analytics features than larger platforms. Customer support has received mixed reviews. Less suited for complex inpatient workflows.

Best for: Tech-forward small-to-mid practices and specialty clinics that prioritize mobile workflows and customizable documentation.

10. Practice Fusion

Practice Fusion is one of the most widely used cloud-based EMR platforms for small ambulatory practices in the US, with a straightforward interface and affordable subscription pricing. It covers clinical documentation, e-prescribing, lab integration, scheduling, and billing.

Strengths: Affordable, easy to learn, cloud-based with minimal setup, solid e-prescribing and lab integration.

Limitations: Less feature depth than mid-market platforms. Has faced regulatory issues in the past – worth reviewing before committing.

Best for: Small practices and solo physicians looking for a straightforward, affordable entry-level EMR.

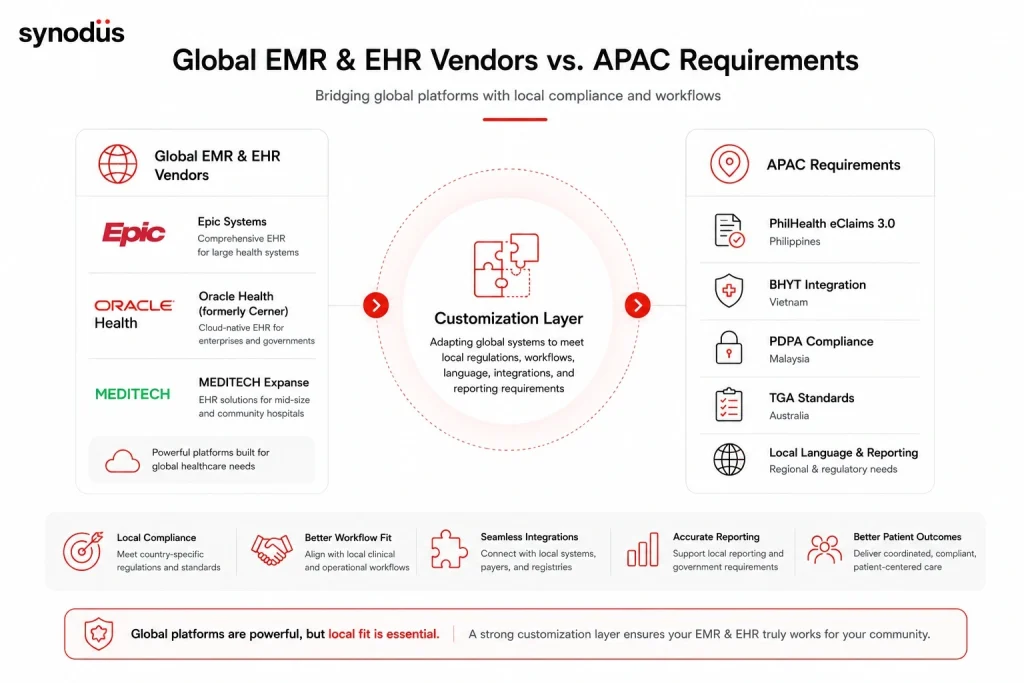

Top EMR and EHR companies for APAC and custom development

Large US vendors like Epic and Oracle are technically deployable in APAC markets, but local compliance requirements – PhilHealth eClaims in the Philippines, BHYT integration in Vietnam, PDPA in Malaysia, TGA standards in Australia – are not built into these products. Getting them to work in those contexts requires substantial custom development on top of an already expensive platform.

For hospitals in Southeast Asia, MENA, and other markets with specific regulatory environments, two options deliver better fit:

Regional OTS products with local compliance built in – examples include Hybrain’s MEDtrix (Philippines), Origin Integrated Studios (Malaysia), and Bizbox (Philippines).

Custom or hybrid development vendors that build compliance into the system architecture from the start.

11. Synodus

Synodus is a Vietnam-based healthcare software development company with 250+ developers and 30+ healthcare implementations across Vietnam, the Philippines, Malaysia, and Australia. Clutch rating: 5.0.

Their hybrid model combines a validated EMR base – covering clinical documentation, medication management, CPOE, lab integration, billing, and scheduling – with custom development for local compliance requirements, specialty workflows, and third-party integrations. This delivers the flexibility of a custom build at lower cost than starting from scratch.

Recent results:

Multi-field hospital complex – 700 beds, 2,500 outpatients and 800 staff daily. Custom EMR with cloud-based records, two-layer encryption, e-prescription, document scanning, and full HIS integration. Built in 4 months. Results: 70% improvement in operational efficiency, 90% decrease in incident rates, 3x faster diagnosis, 85% of patient documents digitalized. Read the full EMR/EHR case study.

Vietnam University Hospital – 5,000 outpatients and 1,700 medical staff daily. Integrated EMR, inventory management, analytics dashboard, and patient mobile app. Results: 300% revenue increase, $70,000/month in administrative cost savings, 0.01% insurance claim denial rate.

Best for: Mid-to-large APAC hospitals with local compliance requirements, complex specialty workflows, or multi-facility deployment needs that US OTS products cannot serve well without significant additional investment.

Head-to-head comparison

| Company | Best for | Deployment | Pricing | Market share / rating |

|---|---|---|---|---|

| Epic | Large hospitals, academic centers | Cloud / On-premise | $15M+ enterprise | 41.3% US acute care |

| Oracle Health | Large systems, government, VA | Cloud-native (OCI) | Enterprise pricing | 21.8% US acute care |

| MEDITECH Expanse | Mid-size, community, rural | Cloud (MaaS) / On-premise | Custom quote | 11.9% US acute care |

| eClinicalWorks | Multi-specialty clinics, outpatient | Cloud | From $449/month | 180,000+ users |

| Athenahealth | Independent practices, ambulatory | Cloud | Custom quote | 160,000+ providers |

| NextGen | Specialty practices, community health | Cloud / On-premise | Custom quote | Strong specialty ratings |

| Veradigm | Multi-site ambulatory networks | Cloud | Custom quote | Mid-market |

| Tebra | Solo and small practices | Cloud | From $299/month | Purpose-built indie |

| DrChrono | Mobile-first small practices | Cloud | From $199/month | iPad-native |

| Practice Fusion | Entry-level small practices | Cloud | From $149/month | Affordable entry |

| Synodus (custom) | APAC hospitals, complex workflows | Custom | From $25/hr | 5.0 Clutch, 30+ APAC |

How to choose between EMR/EHR companies

Step 1: Define your facility type

The right EMR company for a 600-bed academic hospital is completely different from the right one for a 3-physician family practice. Start by being specific about your bed count, specialty mix, and patient volume.

Step 2: Map your compliance requirements

US practices: HIPAA, ONC certification, state-specific requirements. Philippine facilities: PhilHealth eClaims 3.0 certification, DOH EMR standards. Malaysian facilities: PDPA, NPSTI. Vietnamese facilities: MOH data standards, BHYT integration. Any vendor claiming compliance with your local requirements should demonstrate it with documentation.

Step 3: Evaluate fit against your actual workflows

Give vendors realistic “day in the life” scenarios based on your most common clinical situations and ask them to demo those specifically. A vendor who struggles with your actual workflows in a demo will struggle more post-implementation. Before shortlisting vendors, it helps to have a clear picture of what benefits and limitations to expect from any EMR system – see the EMR advantages and disadvantages guide for a data-backed assessment.

Step 4: Verify interoperability

Map every external system you need to connect with – labs, imaging, pharmacy, insurance payers, national health registries. For each, verify the vendor has a live integration in production, not a theoretical API. Poor interoperability is one of the most cited causes of EMR implementation failure.

Step 5: Check total cost of ownership

License or development cost is one line. Implementation, training, data migration, compliance customization, and ongoing maintenance typically add 50-100% on top. Get a full 3-year TCO estimate before comparing vendors on price. For a full cost framework, see the EMR cost guide for clinics and small practices or the EHR cost and ROI breakdown for larger facilities.

FAQs

Epic Systems is the largest EMR company by market share, commanding 41.3% of the US acute care hospital segment. Oracle Health (formerly Cerner) is second at 21.8%, followed by MEDITECH at 11.9%. In the ambulatory practice segment, eClinicalWorks and Athenahealth are among the largest vendors by number of users.

For small and solo practices, Tebra, DrChrono, Practice Fusion, and eClinicalWorks are among the most widely used options. They offer cloud-based deployment, affordable subscription pricing, and interfaces designed for practices without large IT teams. For a full cost comparison, see the EMR price guide for small practices.

No. Epic is the best choice for large health systems with the budget, IT infrastructure, and organizational capacity for a complex, long-term implementation. For mid-size hospitals, MEDITECH Expanse consistently outperforms Epic on cost and implementation manageability. For small practices, eClinicalWorks or Tebra are more practical. For APAC hospitals with local compliance requirements, regional or custom-built systems often deliver better fit than US-centric platforms.

In practice, most vendors use EMR and EHR interchangeably. The technical distinction is that EMR refers to records within a single practice, while EHR implies cross-provider data sharing. Most modern systems marketed as EMR include EHR-style interoperability features. When evaluating vendors, focus on whether the system supports HL7 FHIR for data exchange rather than whether it is labeled EMR or EHR. For a full comparison of the two concepts, see the EMR vs EHR vs PHR guide.

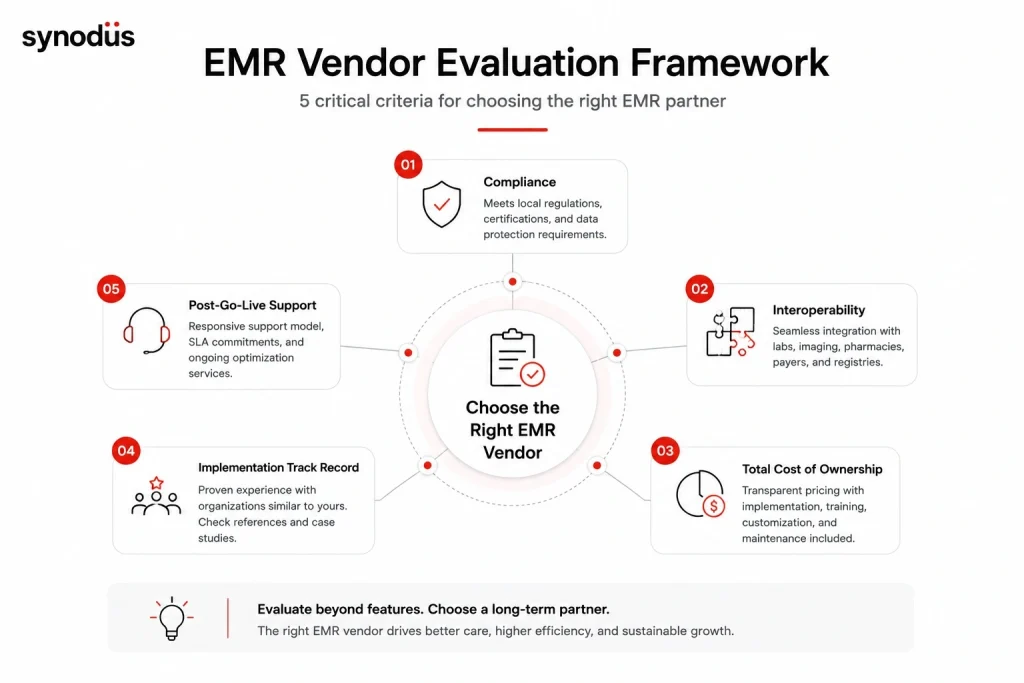

Five criteria matter most: compliance certification for your market, interoperability with your existing systems (verified with live production references, not demos), total cost of ownership over 3-5 years, implementation track record with facilities similar to yours, and post-go-live support model. For a detailed vendor evaluation framework, see the hospital information system companies guide – the evaluation criteria apply equally to EMR vendors.

For APAC hospitals with specific local compliance requirements, US-centric vendors like Epic and Oracle require substantial additional development to meet local standards and are often impractical for facilities outside major metropolitan markets. Regional OTS products with local compliance built in (Hybrain MEDtrix in the Philippines, Origin Integrated Studios in Malaysia) are practical for standard workflows. Custom or hybrid development vendors like Synodus deliver better workflow fit and local compliance coverage for facilities with complex or unique requirements.