Key takeaway

- South Korea recorded a record-low fertility rate of 0.72 in 2023, creating a long-term engineering talent constraint that domestic hiring alone cannot resolve.

- Vietnam’s fintech market is projected to surge from USD 19.35 billion to USD 63.25 billion by 2034 (13-15% CAGR), driven by fundamental shifts in consumer behavior rather than short-term capital.

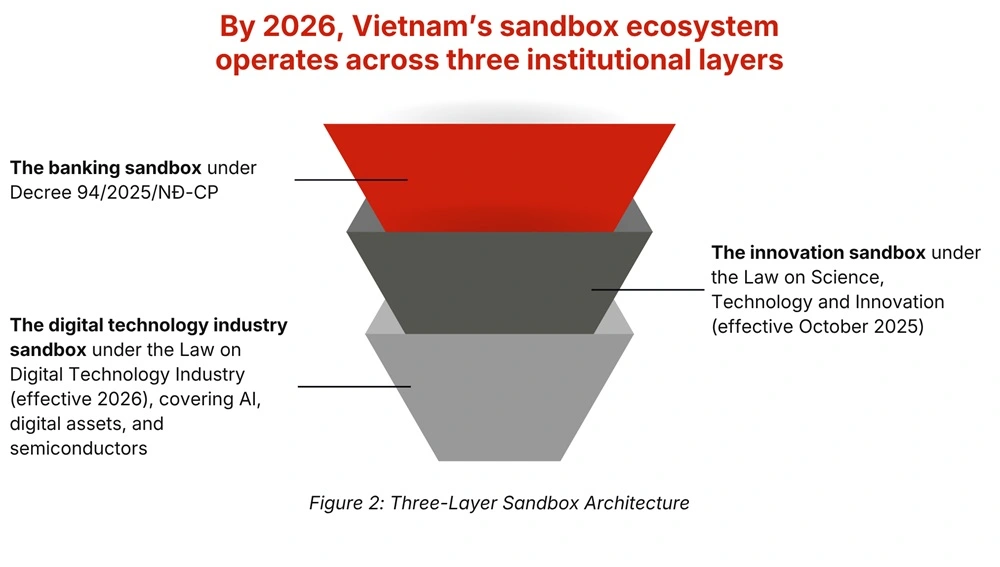

- The regulatory environment has transformed. The fintech sandbox is formally codified (Decree 94/2025/NĐ-CP), Decree 13 provides a clear path for data localization, and the Da Nang International Financial Center is fully operational as of January 2026.

- Korean pioneers like Toss, Lotte Finance, and Webcash have already built defensible moats in Vietnam by identifying gaps the local market failed to close.

The pressure is coming from home first

Before evaluating Vietnam, Korean technology leaders must be clear about what is happening domestically. South Korea’s fertility rate of 0.72 is not a temporary trend. It is a structural shift already severely impacting engineering teams: shrinking junior pipelines, intensifying competition for senior talent, and driving costs across the board.

For companies building or maintaining complex, highly regulated software systems, predictably scaling delivery capacity solely from Korea is becoming structurally harder every year. Hiring your way out of this is not a strategy; it is just a delay.

The market leaders are not waiting for the domestic market to correct itself. They are designing a different supply model, and increasingly, that design leads directly to Vietnam.

What Vietnam actually is in 2026

Many Korean companies evaluate Vietnam purely through a cost-saving lens. That lens misses the most critical picture.

Engineering depth in Vietnam is real. The country produces 100,000 ICT graduates annually. Samsung’s R&D center in Hanoi, its largest in Southeast Asia, represents a commitment exceeding USD 4 billion. These are not short-term, cost-optimization decisions. They are massive infrastructure bets by companies expecting Vietnam to matter for decades.

The market itself is the opportunity. Vietnam’s fintech sector is one of Southeast Asia’s fastest growing. It features a mobile-first consumer base that bypassed traditional credit card infrastructure entirely, moving straight from cash to digital wallets. For Korean fintechs, Vietnam is not just an engineering base; it is a primary revenue market.

Crucially, regulatory clarity now exists. Vietnam’s fintech sandbox is formalized across three legal pillars. Seven domains are explicitly open for licensed testing, including digital payments, eKYC, credit scoring, and open APIs. The compliance risk that paralyzed foreign decision-making two years ago now has a structured path. Vietnam is no longer a regulatory gray zone.

What the early Korean movers understood

Three major Korean companies have already built defensible positions in Vietnam. Their approaches differed entirely, but their underlying logic was identical: Do not compete directly in Vietnam’s saturated segments.

- Toss (Viva Republica): Toss did not enter as a financial services company. They launched a non-financial utility app (step-counter rewards) to build approximately 3 million monthly active users at a fraction of standard financial marketing costs. They only introduced regulated financial products after establishing a massive distribution.

- Lotte Finance: Lotte leveraged proprietary ecosystem data from its Vietnam retail operations to underwrite customers that conventional credit bureaus could not evaluate. This enabled them to process BNPL (Buy Now, Pay Later) approvals in 30 seconds without requiring income documentation.

- Webcash: Webcash ignored the crowded retail fintech market completely. They identified a specific B2B pain point – Korean SMEs in Vietnam struggling with local tax compliance and e-invoicing – and built specialized infrastructure around that exact problem. Their defensibility comes from deep compliance integration, not sheer scale.

None of these companies competed directly in Vietnam’s most saturated segments. Each found the intersection between their existing Korean capability and a gap the local market had not closed.

The full execution detail of each case, including entry strategy, product decisions, and strategic lessons, is covered in our Vietnam Market Guide. Download the full Executive Playbook here

The decision most leadership teams get wrong

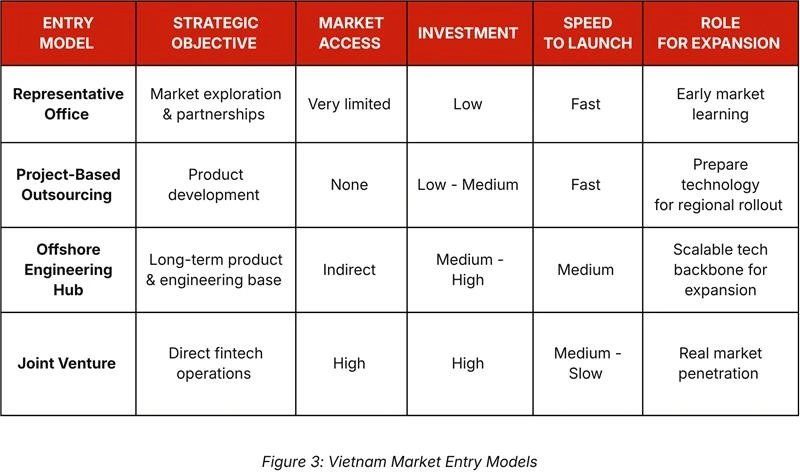

Vietnamese market entry rarely fails because of bad market conditions. It fails because of the wrong entry structure.

Treat expansion as an operating model decision, not a geographic one. Korean companies expanding into Vietnam in 2026 typically must choose between four operating models. Each requires a different balance of investment, control, and speed:

There is no universal answer. The right structure depends on one question: is your primary objective for the first 18 months learning the market, building engineering capacity, or generating local revenue? Getting the structure wrong is more expensive than getting the timing wrong.

How Synodus supports Korean expansion

Synodus is a Vietnam-based technology firm specializing in banking, financial services, and insurance. We are the IT delivery partner for Vietnam’s major financial institutions including Vietcombank, VietinBank, MB Bank, and HDBank, and operate under ISO 27001 and PCI-DSS frameworks.

For Korean fintech and software companies, we provide three mission-critical capabilities:

- Regulatory compliance architecture from day one: We integrate Decree 13 data localization requirements, sandbox compliance structures, and financial security standards directly into system design – not as a post-deployment retrofit.

- Engineering delivery built for financial systems: Our teams have production experience with the specific constraints of Vietnamese financial infrastructure – core banking integration, eKYC systems, payment rails, and audit requirements that generic outsourcing vendors do not carry.

- Local institutional relationships: We work alongside the banks, regulators, and technology partners that Korean firms need to navigate – reducing the time and friction between market entry decision and operational deployment.

The cost of waiting is not abstract

The companies already succeeding in Vietnam did not wait to see how the market developed. They developed it. Toss’s massive user base was not built overnight. Lotte Finance’s data advantage took years to accumulate. Webcash’s compliance depth cannot be replicated quickly by a hesitant new entrant.

These operational advantages compound every single quarter they hold them.

The question for Korean technology leaders in 2026 is no longer whether Southeast Asia is strategically relevant. The structural pressures in Seoul and the massive opportunities in Hanoi make the direction obvious. The real question is whether you will arrive with a deliberate, structured entry model, or whether you will arrive after a competitor has already taken the defensible positions.

The companies that succeed in Vietnam this year will not necessarily be those with the biggest budgets. They will be the ones who truly understood the market before they committed to it.

Unlock Your Expansion Blueprint

We built a comprehensive, 30-page practical guide for Korean fintech and software leaders making this exact decision in 2026.

Inside the Playbook, you will find:

- Vietnam’s 2026 regulatory environment decoded (Decree 13 & The Sandbox).

- Detailed assessments of the 6 major Fintech segments with immediate Korean opportunity.

- In-depth case studies of Toss, Lotte Finance, and Webcash.

- A strict framework for choosing the exact entry model for your specific business objectives.